UK house prices slipped in March with the latest Halifax index pointing to a loss of momentum as rising mortgage costs and macro uncertainty begin to bite.

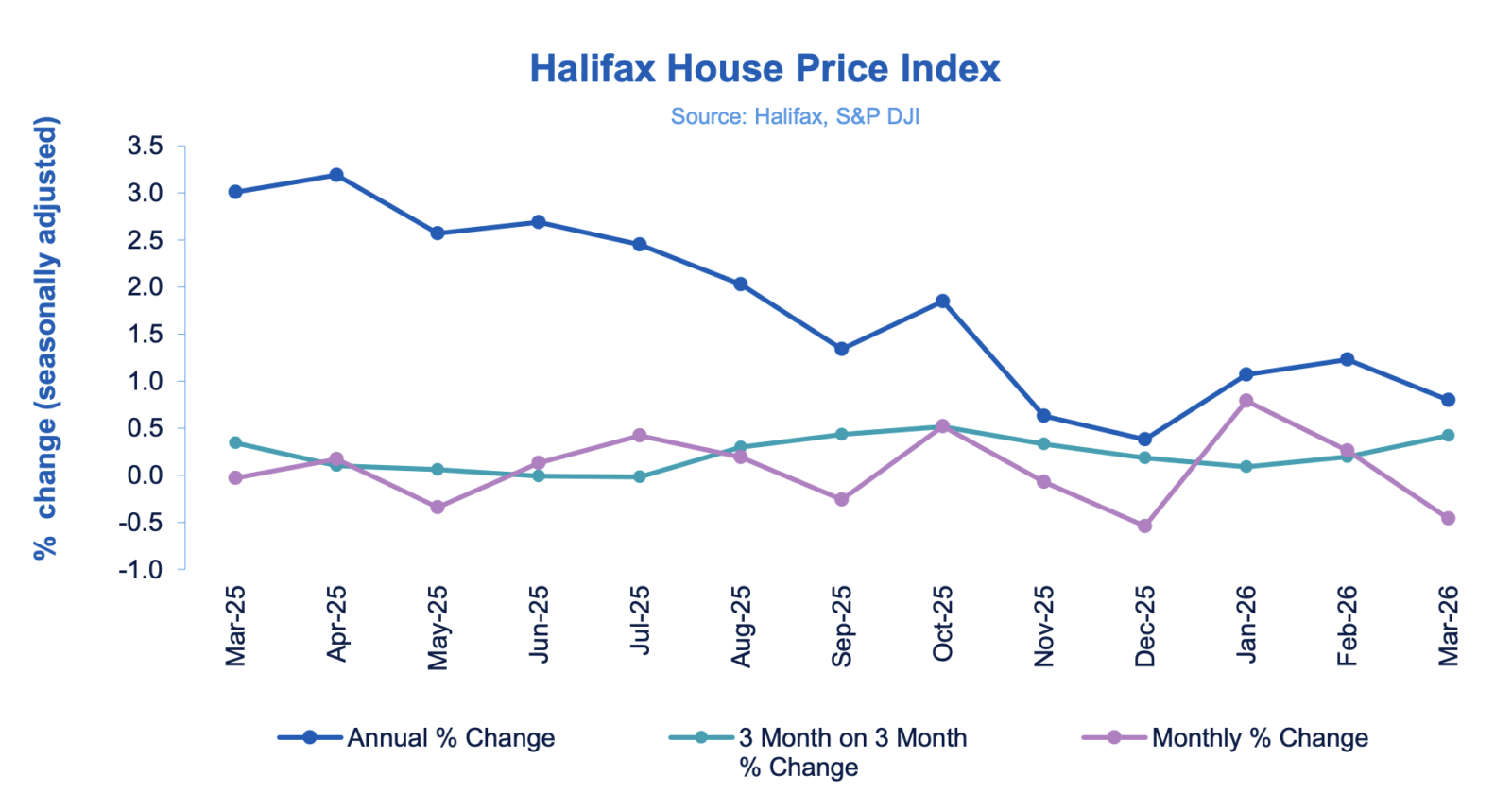

Average values fell by -0.5% during the month, reversing February’s +0.3% increase, taking the typical UK house price to £299,677.

Annual growth also eased to +0.8% from +1.2%, suggesting the market’s early-year resilience is starting to fade as spring activity gets underway.

For the specialist finance sector, the shift is likely to translate into more cautious borrower behaviour, with transactions slowing and increased reliance on short-term funding to bridge gaps in chains and refinancing strategies.

The slowdown comes amid renewed volatility in global markets, with rising energy prices and inflation expectations pushing mortgage rates higher and dampening expectations of near-term base rate cuts.

NORTH SOUTH DIVIDE

Northern Ireland continues to lead with annual growth of +8.7%, followed by Scotland at +4.4% and Wales at +1.6%.

Across England, growth is concentrated in more affordable regions, with the North East up +5% and the North West rising +3.1%.

In contrast, southern markets are under pressure, with the South East down -1.9% year-on-year and London slipping by -1.2%, reflecting ongoing affordability constraints and reduced buyer demand.

The data points to a market that remains stable on the surface but increasingly sensitive to shifts in funding costs — a dynamic that typically drives greater demand for bridging solutions, particularly where speed and flexibility are required.

MIDDLE EAST UNCERTAINTY

Amanda Bryden (main picture, inset), Head of Mortgages at Halifax, says: “House prices fell -0.5% in March, following the modest +0.3 per cent increase seen in February. As a result, the average property price is now £299,677. The pace of annual growth has also eased, slowing to +0.8 per cent from +1.2 per cent the previous month, suggesting the market has lost some momentum as spring begins.

“The recent slowdown in the housing market reflects the wide uncertainty regarding the conflict in the Middle East. Concerns about higher energy prices have pushed up inflation expectations, which in turn led to a rise in mortgage rates, reducing confidence that interest rates will be cut this year and dampening the initial momentum in the market seen at the start of the year.”

PRICES MAY PROVE RESILIENT

She adds: “The effect on house prices will largely depend on how long-lasting these pressures prove to be and the wider implications for the economy and unemployment. Mortgage rates are a key factor for buyers, particularly those getting on the ladder for the first time, who are already balancing the challenge of saving a deposit, with the cost of borrowing.

“However, the recent increase in UK mortgage rates has been more modest than the sharp rises seen during the mini budget of 2022. Further, many households will already be on fixed deals, protecting them from the latest rate rises. Taking all this into account, house prices may prove resilient, even if uncertainty weighs on market activity in the near term.”

STAMP DUTY HOPES FADE

Tomer Aboody, director of specialist lender MT Finance, says: “The housing market saw a small bounce at the end of last year and into this one once the Budget was out of the way as buyers and sellers felt more confident about their prospects.

“Although hope of lower rates and stamp duty are dwindling, many have already come to the conclusion that there is only so long they can put off the decision to move before they simply have to because of their situation.

“The data suggests that many have waited for so long that they are pressing on regardless of the Middle East conflict and pressures that places on our economy.”

FUTURE CHALLENGES

Nathan Emerson, CEO of Propertymark, adds: “We are at an important intersection where we must clearly acknowledge future challenges ahead. We started the year with positivity in terms of seeing an uplift in the average number of viewings per available property, coupled with general consumer positivity regarding affordability.

“However, a lot has changed in a short space of time, with numerous sub 4% mortgage deals being withdrawn over the last few weeks as the wider economy adjusts to potential uncertainties.

“Inflation is expected to increase over the coming months and this is likely to have an immediate effect on consumer affordability.

“The rate of inflation will also play intense influence on the Bank of England regarding base rate decisions over the forthcoming months too.

“In addition, we are also due to see OFGEM make their next decision regarding energy price caps late next month, which again should be highly considered regarding household affordability as the year plays out.”